Understanding Financial Planning and Business Transitions

The decision to transition a business is one of the most significant an owner will ever make, impacting not only their personal financial future but also the lives of employees, the legacy of the company, and even the vitality of the local community. Without proper foresight and strategic planning, the risks of a failed succession are substantial. As highlighted by recent data, an estimated 30% of small business closures result from inadequate succession planning. This statistic underscores a critical need for business owners to engage in comprehensive transition planning, moving beyond the day-to-day operations to proactively shape their future exit.

A successful transition is not merely a transaction; it’s a carefully orchestrated process that integrates financial, legal, and emotional considerations. Many owners face a significant psychological hurdle when contemplating their exit, as their identity is often deeply intertwined with their business. Addressing this psychological readiness is as crucial as the financial preparations. For those seeking to define a successful exit beyond just the numbers, exploring resources like Beyond the Business: Defining Your Successful Exit can offer invaluable perspective on aligning personal aspirations with business outcomes.

What is Business Transition Planning?

Business transition planning, often interchangeably referred to as exit planning or succession planning, is a strategic process designed to prepare a business and its owner for a future change in leadership, ownership, or both. It encompasses a wide array of considerations, including:

- Leadership Succession: Identifying and developing future leaders to ensure the company’s operational continuity and smooth management transfer. This involves mentoring, training, and sometimes bringing in external talent.

- Ownership Transfer: Determining how the ownership stake will be transferred, whether through a sale to a third party, an internal transfer to family or employees, or other structures. This is where the financial value of the business is realized by the owner.

- Asset Preservation: Strategies to protect the value of the business and its assets throughout the transition process, ensuring that the owner’s wealth is maximized and secured.

- Corporate Governance: Establishing robust governance structures that can withstand leadership changes and ensure the long-term health and stability of the organization.

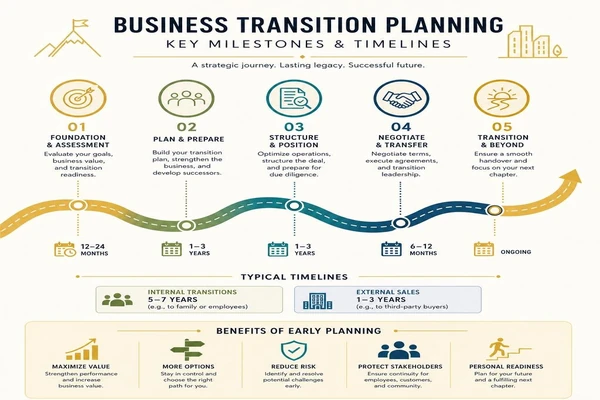

The goal of business transition planning is to maximize the value of the business at the point of transfer, minimize tax implications, ensure a smooth handover, and enable the owner to achieve their personal and financial objectives post-transition.

Why Early Preparation is Essential

Despite the clear benefits, a staggering statistic reveals that only an estimated 33% of U.S. small businesses have a formal transition plan in place. This lack of preparation is a primary driver of the high failure rate in business successions. The complexity of these transitions demands significant lead time, far more than many owners anticipate.

For instance, internal transitions, such as selling to employees or family members, often require a timeline of five to seven years. This extended period allows for the development of successors, the gradual transfer of knowledge and responsibilities, and the structuring of financial arrangements that may involve seller financing or earn-outs. In contrast, external sales to third parties, while potentially quicker, still typically demand one to three years of meticulous planning to prepare the business for market, conduct due diligence, and negotiate terms.

Starting early provides several critical advantages:

- Value Maximization: It allows time to identify and address weaknesses, implement value-building strategies, and optimize the business’s financial performance.

- Flexibility: Owners have more options and are not forced into a suboptimal exit strategy due to time constraints or unforeseen circumstances.

- Risk Mitigation: Early planning helps identify potential legal, tax, or operational hurdles, allowing ample time to resolve them.

- Personal Readiness: It gives the owner time to mentally and emotionally prepare for life after the business, which is often a significant adjustment.

Delaying this process can lead to rushed decisions, reduced business value, increased tax burdens, and potential disruption for employees and customers. A proactive approach is the cornerstone of a successful and financially rewarding transition.

Evaluating Your Transition Pathways

Once the decision to transition has been made, business owners face a critical choice: which pathway best aligns with their goals? There is no one-size-fits-all solution, and understanding the various options is paramount. These pathways range from internal transfers to employees or family members to external sales to strategic or financial buyers. Each option comes with its own set of advantages, challenges, and implications for the business, its employees, and the owner’s financial outcome. For a comprehensive overview of the possibilities, exploring resources like The Ultimate List of Business Exit Strategies can be an excellent starting point.

Internal Successions: Family and Employees

Internal successions involve transferring ownership or leadership to individuals already connected with the business, typically family members or employees. These options often appeal to owners who prioritize preserving the company culture, ensuring continuity, and rewarding loyal team members.

- Family Transitions: Transferring the business to a son, daughter, or other relative is a deeply personal choice, often driven by a desire to continue a family legacy. However, these transitions come with unique complexities, including managing family dynamics, ensuring fairness among heirs (both active and non-active in the business), and preparing the next generation for leadership. Unfortunately, the success rate for family-owned businesses transitioning to the second generation has declined to as low as 19% in recent years, highlighting the challenges involved. Proper planning must address not only business operations but also family governance and communication structures.

- Employee Stock Ownership Plans (ESOPs): An ESOP is a qualified retirement plan that allows employees to own shares in the company. This option offers significant tax advantages for both the owner and the employees, fosters employee engagement, and can create a built-in market for the owner’s shares. ESOPs are particularly attractive for owners who wish to sell a portion or all of their equity while maintaining a degree of control and ensuring the company remains independent.

- Management Buyouts (MBOs): In an MBO, the existing management team purchases the business from the owner. This option leverages the management team’s intimate knowledge of the company and its operations, often leading to a smooth transition. MBOs can be financed through a combination of the management team’s capital, seller financing, and external debt.

Internal successions generally require a longer planning horizon, often five to ten years, to adequately prepare successors, structure financing, and navigate the intricate personal and professional relationships involved.

External Sales: Strategic and Financial Buyers

External sales involve selling the business to a third party not currently associated with the company. These options are typically focused on maximizing the sale price and providing a clean break for the owner.

- Strategic Buyers: These are often larger companies in the same or a related industry that acquire businesses to gain market share, expand product lines, eliminate competition, or achieve synergistic benefits. Strategic buyers are often willing to pay a premium for businesses that complement their existing operations and offer clear growth opportunities.

- Financial Buyers: This category primarily includes private equity firms, venture capitalists, or individual investors who acquire businesses with the intent to grow them and sell them for a profit within a specific timeframe (typically three to seven years). Financial buyers focus heavily on the business’s financial performance, growth potential, and the strength of its management team. They often look for businesses with stable cash flows, strong market positions, and opportunities for operational improvements.

- Recapitalization: This involves changing the capital structure of the company, often by taking on new debt to pay a dividend to shareholders (the owner). This allows the owner to take some liquidity out of the business while retaining a significant ownership stake.

External sales can offer a quicker path to liquidity and often result in a higher sale price, particularly for well-prepared businesses with strong financial performance. However, they may involve a loss of control over the company’s future direction and culture.

Here’s a simplified comparison of internal and external transition options:

Feature Internal Transitions (Family/Employees) External Sales (Strategic/Financial) Primary Goal Preserve legacy, culture, employee well-being, gradual exit Maximize sale price, clean break, faster liquidity Timeline Longer (5-10+ years for preparation) Shorter (1-3 years for preparation and sale) Buyer Type Known entities (family members, existing employees/management) Unknown entities (competitors, investment firms, individual investors) Valuation Often negotiated, may involve seller financing or non-cash considerations Market-driven, typically cash-based, higher multiples for synergies Control Owner may retain some involvement/influence post-transition Owner typically relinquishes full control post-sale Complexity Emotional, family/employee dynamics, financing for internal buyers Due diligence, legal negotiations, market timing, confidentiality Tax Impact Can be structured for long-term tax efficiency (e.g., ESOPs, gifting) Focus on capital gains, potential for immediate large tax event Choosing the right path requires careful consideration of personal goals, business readiness, and market conditions. Each option demands a tailored approach and a dedicated team of advisors to navigate its intricacies.

Aligning Personal Wealth with Corporate Exits

For many business owners, their company represents not just a source of income, but their primary asset and the cornerstone of their personal wealth. This concentration of wealth in an illiquid asset creates a unique financial planning challenge. A successful business transition is fundamentally about converting this enterprise value into personal financial security, ensuring that the owner’s post-exit lifestyle and retirement needs are met. This requires a meticulous alignment of personal financial goals with the business exit strategy.

Often, owners have a “wealth gap” – the difference between their current net worth (including business value) and the amount needed to fund their desired lifestyle and retirement. Bridging this gap is central to transition planning, as it dictates the minimum sale price or liquidity event required from the business. It’s not enough to simply sell the business; the proceeds must be sufficient to sustain the owner’s desired future, whether that involves retirement, new ventures, or philanthropic endeavors.

Bridging the Valuation Gap

Understanding the true market value of your business is a critical first step. Owners often have an emotional attachment that can lead to an inflated perception of their company’s worth. However, buyers base their valuations on objective metrics. Most middle-market businesses are valued using a multiple of their Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). This EBITDA must be “normalized” by adding back discretionary expenses or one-time costs that would not be incurred by a new owner, providing a clearer picture of the business’s true earning power.

The “valuation gap” isn’t just about the current worth versus the desired worth; it’s also about the difference between a perceived value and what the market is actually willing to pay. Factors like customer concentration, management depth, and recurring revenue models significantly influence this multiple. To truly bridge this gap, owners must understand these drivers and proactively work to enhance them. For a deeper dive into how businesses are valued and what drives that value, exploring resources like The Ultimate Guide to Business Valuation can provide essential insights. The ultimate goal is to ensure that the net-of-tax proceeds from the transition are sufficient to fund the owner’s next chapter.

Integrating Financial Planning and Business Transitions for Retirement

Retirement planning for a business owner is inextricably linked to their business transition. Unlike employees with defined contribution plans, a significant portion of an owner’s retirement nest egg is tied up in their company. Therefore, the business exit is the retirement plan.

Key considerations include:

- Retirement Readiness: Calculating the exact amount of capital needed to sustain a desired post-exit lifestyle, factoring in inflation, healthcare costs, and longevity.

- Post-Exit Identity: Many owners struggle with the psychological shift of no longer being “the boss.” Financial planning should include strategies for engaging in new activities, hobbies, or philanthropic work to maintain purpose and fulfillment.

- Cash Flow Analysis: Developing a detailed cash flow projection for life after the business, ensuring that investment income and other sources of funds will cover expenses.

- Estate Planning: Integrating the business transition into a broader estate plan to ensure wealth is distributed according to the owner’s wishes, minimizing estate taxes, and providing for future generations.

A holistic approach ensures that the business transition serves as a catalyst for a secure and fulfilling retirement, rather than an abrupt and unprepared departure.

Mitigating Risks with Life Insurance for Business Transitions

Business transitions, by their very nature, involve significant risks that can be mitigated through strategic use of life insurance. This financial tool plays a crucial role in protecting the business, its owners, and their families during unforeseen circumstances.

- Buy-Sell Agreements: Life insurance is often the funding mechanism for buy-sell agreements. These legal contracts dictate how a deceased or disabled owner’s share of the business will be purchased by the remaining owners or the company itself. Without insurance, the surviving owners might lack the capital to buy out the deceased’s heirs, potentially forcing a sale of the business or creating financial hardship for the family.

- Key-Person Coverage: If the business relies heavily on a “key person” (often the owner), life insurance can provide financial protection if that individual dies or becomes disabled. The proceeds can help the company cover operational losses, recruit a successor, or pay off debts, ensuring business continuity during a critical period.

- Estate Tax Liquidity: For owners of highly valuable businesses, estate taxes can be a significant burden on their heirs. Life insurance can provide the necessary liquidity to pay these taxes without forcing the sale of the business or other illiquid assets at a discount.

For comprehensive guidance on how to leverage this vital tool, exploring resources on Life insurance for business transitions can provide tailored solutions to protect your legacy and financial future. Properly structured life insurance policies are an essential component of a robust transition plan, safeguarding against the unexpected and ensuring that the owner’s legacy and family are protected.

Key Financial, Legal, and Tax Considerations

A successful business transition is a complex dance of financial optimization, legal precision, and tax efficiency. Overlooking any of these pillars can significantly erode the value realized by the owner and create unforeseen liabilities. From the moment an owner contemplates an exit, every decision must be viewed through these critical lenses to ensure maximum value retention and a smooth handover.

Tax Mitigation Strategies and Deal Structuring

Taxes are often the single largest expense in a business sale, making strategic tax planning indispensable. The structure of the deal-whether it’s an asset sale or a stock sale-can have vastly different tax implications for both the seller and the buyer.

- Capital Gains: The primary goal for sellers is often to maximize long-term capital gains treatment, which is typically taxed at a lower rate than ordinary income.

- QSBS Section 1202: For qualifying small businesses, Section 1202 of the Internal Revenue Code allows for a significant exclusion of capital gains tax on the sale of Qualified Small Business Stock (QSBS), potentially up to $10 million or 10 times the adjusted basis of the stock. Understanding and planning for this exclusion can be a game-changer.

- Gifting Strategies (GRATs, IDGTs): For owners planning to transfer wealth to family members, sophisticated gifting strategies like Grantor Retained Annuity Trusts (GRATs) and Intentionally Defective Grantor Trusts (IDGTs) can be used to move business interests out of the taxable estate, minimizing future estate taxes.

- Asset vs. Share Sales: In an asset sale, the buyer purchases individual assets of the business, which can offer tax benefits to the buyer (depreciation deductions). In a share sale, the buyer acquires the company’s stock, which is generally more tax-efficient for the seller (capital gains treatment). The negotiation often involves balancing these opposing tax interests.

Working with experienced tax advisors early in the process is crucial to structure the deal in the most tax-efficient manner possible, preserving more of the hard-earned proceeds.

Operational Readiness and the Valuation Process

The financial value of a business is not solely determined by its current profitability but also by its operational strength and future potential. Buyers are looking for businesses that are well-run, scalable, and not overly dependent on the owner.

- Customer Concentration: A business that relies heavily on one or a few major customers is perceived as riskier. Diversifying the customer base reduces this risk and enhances value.

- Management Depth: A strong, autonomous management team that can run the business without the owner’s daily involvement is a significant value driver. This demonstrates continuity and reduces buyer risk.

- Recurring Revenue: Businesses with predictable, recurring revenue streams (e.g., subscriptions, service contracts) are highly attractive to buyers as they offer stability and forecastable cash flows.

- Clean Financials: Buyers will conduct extensive due diligence. Having three to five years of clean, audited or reviewed financial statements is non-negotiable. Any discrepancies or lack of transparency will raise red flags and can derail a deal or significantly reduce the valuation.

Beyond these internal factors, the efficiency of your business marketing process also plays a role in operational readiness. A well-oiled marketing machine that consistently generates leads and builds brand equity makes the business more attractive and demonstrates its growth potential to prospective buyers. A robust and efficient business marketing process signals a healthy, forward-looking enterprise.

The Role of Professional Advisors in Financial Planning and Business Transitions

Navigating the complexities of a business transition is rarely a solo endeavor. A team of highly specialized professional advisors is indispensable for maximizing value, mitigating risks, and ensuring a smooth process.

- Fiduciary Advisors: A fiduciary financial advisor, legally and ethically bound to act in the client’s best interest, provides integrated oversight across all aspects of the transition. They help align personal financial goals with the business exit, coordinate other advisors, and ensure a holistic approach to wealth management.

- CPAs (Certified Public Accountants): Essential for tax planning, financial statement preparation, and ensuring compliance. They help structure the deal to minimize tax liabilities and provide accurate financial data for valuation and due diligence.

- Transaction Attorneys: These legal experts draft and negotiate the complex legal documents involved in a business sale, including letters of intent, purchase agreements, and non-compete clauses. They protect the owner’s interests and ensure legal compliance.

- M&A Advisors (Mergers & Acquisitions Advisors) / Business Brokers: These professionals specialize in valuing businesses, identifying pool of potential buyers, marketing the business confidentially, and managing the sale process from start to finish. They act as intermediaries, negotiating on behalf of the seller.

- Business Valuators: Independent valuators provide an objective assessment of the business’s worth, which is crucial for setting a realistic asking price and for tax and estate planning purposes.

These advisors work collaboratively, forming a cohesive team that guides the owner through every stage of the transition. As businesses evolve, so do the needs of their owners, requiring advisors to adapt their approach. Insights from experts, such as those discussed in How To Better Help Business Owner Clients On The Stage Of Their Journey, emphasize the importance of advisors understanding the unique stages of a business owner’s journey to provide truly impactful guidance. Their collective expertise is vital for navigating the intricate financial, legal, and emotional landscape of a business transition.

Frequently Asked Questions about Business Transitions

Business owners often grapple with similar questions when contemplating a transition. Addressing these common concerns can help demystify the process and highlight the critical areas requiring attention.

When is the ideal time to start planning for a business transition?

While there’s no single “perfect” moment, the consensus among experts is that earlier is always better. Ideally, owners should begin planning three to five years before their anticipated exit date. This timeframe provides a crucial runway to:

- Address Operational Red Flags: Sufficient time allows for improvements in management depth, customer diversification, and the implementation of scalable systems that increase business value.

- Optimize Financials: It enables owners to clean up financial records, improve profitability, and establish a track record of strong performance, all of which are critical for valuation.

- Personal Readiness: It gives the owner time to mentally prepare for life after the business and ensure their personal financial plan aligns with their post-exit goals.

Some advisors even suggest a ten-year strategic window for comprehensive planning, especially for internal transitions or those involving complex family dynamics. This extended period allows for gradual leadership development, sophisticated tax planning, and the cultivation of a robust company culture that can thrive post-owner. Delaying planning until an urgent event arises-such as burnout, health issues, or an unsolicited offer-often results in a rushed process, reduced value, and suboptimal outcomes.

What are the “Five Ds” that force unplanned business exits?

Many business transitions are not planned years in advance but are instead triggered by unforeseen circumstances. These events, often referred to as the “Five Ds,” can force an owner to exit their business prematurely and under less-than-ideal conditions:

- Death: The unexpected passing of a key owner or partner can leave a business in turmoil, especially without a clear succession plan or buy-sell agreement funded by life insurance.

- Disability: A severe illness or injury that incapacitates an owner can halt operations or force a rapid sale, often at a discounted price, if no contingency plan is in place.

- Divorce: Marital dissolution can necessitate the division of business assets, potentially leading to forced sales, buyouts, or significant operational disruption.

- Distress: Economic downturns, industry shifts, or severe operational challenges can push a business into financial distress, forcing an owner to sell under pressure or even liquidate.

- Disagreement: Conflicts among partners, family members, or key shareholders can become irreconcilable, leading to a forced separation or sale of interests to resolve disputes.

These “Five Ds” highlight the critical importance of proactive planning, even when an exit seems far off. Contingency plans, robust legal agreements, and adequate insurance can help mitigate the devastating impact of these unplanned events.

How do family dynamics affect succession planning?

Family dynamics introduce a unique layer of complexity to business succession planning, often intertwining emotional, financial, and relational considerations. While family businesses represent a significant portion of the economy, their transitions are notoriously challenging.

- The Three-Circle Model: This widely recognized framework illustrates the overlapping roles in a family business: family, ownership, and management. Conflicts often arise when these circles are not clearly defined, leading to confusion over roles, responsibilities, and decision-making authority.

- Fairness Planning: A common pitfall is equating “fairness” with “equality” among children, regardless of their involvement in the business. Active heirs who dedicate their careers to the company often expect a greater share of ownership or control, while non-active heirs may expect equal financial distribution. Fairness planning seeks to balance these expectations, sometimes through non-business asset allocation or life insurance for non-active children.

- Active vs. Non-Active Heirs: Deciding who will lead the business and how to compensate those not involved can create significant tension. Clear communication, transparency, and professional mediation are essential to navigate these discussions.

- Emotional Attachment: Founders often struggle to relinquish control, viewing the business as an extension of themselves. This emotional attachment can delay decision-making and hinder the development of the next generation.

Successful family transitions require open communication, clearly defined roles, professional governance structures, and a willingness to address difficult conversations early. The goal is not just to transfer a business but to preserve family harmony and legacy for generations to come.

Conclusion

The journey of building a successful business is a testament to an owner’s vision, dedication, and resilience. However, the ultimate measure of that success often lies in the thoughtful execution of its transition. As we move further into June 2026, the imperative for strategic financial planning and business transitions has never been greater, driven by a generational shift in ownership and the profound impact these decisions have on individuals, families, and communities.

A well-executed transition plan is more than just a financial transaction; it is a roadmap to securing both financial independence and a lasting personal legacy. By proactively addressing the complexities of leadership succession, ownership transfer, and wealth preservation, owners can ensure their life’s work continues to thrive, employees are protected, and their personal aspirations for life after the business are fully realized.

The path to a successful exit is paved with early preparation, informed decision-making, and the invaluable guidance of a dedicated team of professional advisors. By understanding the various transition pathways, aligning personal financial goals with corporate strategies, and meticulously addressing legal, tax, and operational considerations, business owners can navigate this pivotal moment with confidence. The time to plan is now, ensuring that the transition from your business is as successful and rewarding as the journey of building it.

{kind=link}